The latest reports from Glenigan, one of the construction industry’s leading insight and intelligence experts, indicates that project-starts returned to decline in July as construction materials inflation continues to accelerate.

On a slightly more positive note, both underlying main contract awards and detailed planning approvals strengthened during the second quarter of 2022, but ultimately remained lower than a year ago.

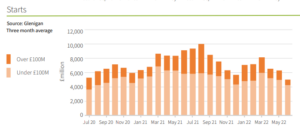

The July review highlights the industry’s disappointing return to decline, as work commencing on-site declined 38% against the preceding quarter to stand 45% lower than the same time in 2021.

July saw the value of major project-starts (over £100 million in value) falter, plummeting 65% against the preceding quarter with a substantial drop of 77% compared with a year ago.

This decline can be largely attributed to ongoing supply chain issues, prompted by the Russia-Ukraine war. The ongoing conflict, which shows little sign of easing in the short term, has accelerated materials inflation, creating an industry stumbling block which it will take time to surmount.

A similarly dismal picture was painted for main contract awards, which fell 2% against the preceding quarter and 11% against the previous year, stagnating the strong pipeline of development contract awards lined up since the pandemic.

Despite an increase in underlying contract awards (7%) against the preceding quarter, the value decreased 6% compared to a year ago. Again, whilst major contract awards also increased against the preceding quarter (+10%), they fell back 22% against the same period a year ago.

Detailed planning approvals fell back 14% against the preceding quarter, and 21% against 2021. This drop was largely influenced by major project approval levels which fell by a third against the preceding quarter and 29% on a year ago. Whilst underlying rose 5% on the previous quarter, it was not enough to reverse the overall decline in this category receding 18% against the previous year.

Sector Analysis – Residential

Underlying performance across sector verticals was a Curate’s Egg. There were some bright spots for residential construction, with the overall value rising 17% in Q.2 compared to Q.1, despite falling back 21% against the previous year.

Work starting on-site for private housing rose significantly on the previous quarter experiencing an overall increase of 43%, buoyed by a rush of work initiated by developers ahead of new building regulations. However these figures remained 14% lower than 2021 levels

Work starting on-site for private housing rose significantly on the previous quarter experiencing an overall increase of 43%, buoyed by a rush of work initiated by developers ahead of new building regulations. However these figures remained 14% lower than 2021 levels

Social housing project-starts performed particularly poorly, slipping back 42% against the preceding quarter as well as 2021.

Sector Analysis – Non-Residential

Performance in the non-residential sector was predominantly negative, holding back any form of recovery.

Civil engineering performed particularly poorly, down 47% against the previous year, with the value of project-starts experiencing a significant decline against the preceding quarter, falling back 27%.

Drilling deeper, the utilities sub-vertical suffered the weakest period of any sector, with project-starts dropping 30% during Q2, standing at almost half (-48%) the value of the previous year; this represented the strongest decline registered against 2021.

Industrial project-starts fell by a quarter against the previous year, registering the greatest quarterly decline (-36%) of any non-residential sector. Health construction starts remained unchanged on Q.1, but also fell by a 25% compared with a year ago.

Drilling into the figures, retail was the only non-residential sector to achieve growth against the preceding quarter, with a modest 6% rise despite project-starts coming in at nearly a third lower than a year ago (-28%).

Drilling into the figures, retail was the only non-residential sector to achieve growth against the preceding quarter, with a modest 6% rise despite project-starts coming in at nearly a third lower than a year ago (-28%).

Hotel & Leisure and Education experienced strong declines during Q2 to stand 40% and 37% lower than a year ago, respectively. Further, both registered a value decrease of 32% and 21% compared with the preceding quarter.

Office starts declined 23% against the preceding quarter, as well as 30% compared with the same period last year.

Regional Analysis

UK Regional performance in Q.2 was incredibly mixed. Positively, the two northern most regions of England performed well.

The North East saw a value increase of 7%, and the North West seeing growth of 2% against the preceding quarter. Mercurially, while project-starts were up 2% against the previous year in the North West, the North East experienced a value decrease of 2% against the same period.

Northern Ireland also posted strong results, experiencing a growth of 3% against the preceding quarter and a significant 44% growth compared with 2021.

The South West also experienced an increase of 11% in Q2, despite project-starts remaining a third lower than the previous year. In the East Midlands, levels remained unchanged against the preceding quarter but experienced the greatest decline (-47%) against the previous year.

London performed particularly poorly, falling a third against the preceding quarter (-30%) to stand 45% lower than a year ago. Yorkshire & Humber also fared poorly, suffering the heaviest decline of any region to stand 32% lower than the preceding quarter, with a 43% value decrease compared with the year before.

Commenting on the findings, Glenigan’s economic director, Allan Wilen, says, “The slight uptick in project-starts reported in last month’s review has unfortunately been superseded by a more negative outlook for July’s edition.

“Project-starts have unfortunately returned to decline as the industry continues to suffer from the fallout of the Russia-Ukraine war, especially the effects of rapidly accelerating construction materials inflation.

“Clearly, the sector is some ways off the levels of recovery seen this time in 2021, but I am cautiously optimistic that signs of strengthening underlying main contract awards and detailed planning approvals point to a development pipeline which is sure to boost levels going into the second half of 2022.”

To find out more about Glenigan, its expert insight and leading market analysis, click here.

{kind=link}