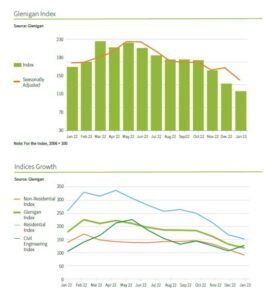

The central finding of the February Construction Review from Glenigan, one of the construction industry’s leading insight and intelligence experts, is that construction-starts remained weak throughout the three months to January, with main contract awards and detailed planning approvals also slumping as the UK continues to weather persistent economic downturn.

Sustained external pressures on the UK construction industry are the main contributing factor to this disappointing performance. This includes rising interest rates on the home front, inflated building materials prices, and rocketing energy costs caused by the Russia-Ukraine conflict. However, some of the decisions taken by the UK Government in the latter half of 2022 are also to blame, denting investor and consumer confidence, eventually resulting in recession.

The sharp fall in project-starts by almost half (-47%) compared to the preceding three months’ performance and a third lower than a year ago is indicative of the above. This was echoed throughout the construction pipeline.

Main contract awards dropped 21% against the preceding period, to stand 16% lower than the same time a year ago. Detailed planning approvals also fell back against the preceding three months (-17%) to finish flat against the year before.

However, the February Review glimpsed a couple of bright spots amongst the gloom. While the value of major project contract awards did fall 31% against the preceding three months, the value increased by almost a fifth (17%) against the previous year. Similarly, major planning approvals were up by over a third (34%) on 2022 levels. This suggests the green shoots of recovery are tentatively starting to appear, even if a full recovery to pre-COVID levels is a little further away on the horizon.

However, the February Review glimpsed a couple of bright spots amongst the gloom. While the value of major project contract awards did fall 31% against the preceding three months, the value increased by almost a fifth (17%) against the previous year. Similarly, major planning approvals were up by over a third (34%) on 2022 levels. This suggests the green shoots of recovery are tentatively starting to appear, even if a full recovery to pre-COVID levels is a little further away on the horizon.

Comments Glenigan’s Economic Director, Allan Wilen: “Starts on site are softening and, as global and national disruption continues, we’ll likely see contractors adopting a cautious and retrenched approach, pushing back start dates until the economic landscape looks less hostile. Rising mortgage rates, falling real wages and poor consumer confidence is likely to cause a further downturn in activity, but that’s not all. Many built environment professionals are still getting to grips with recently introduced regulations, particularly Part L of the Future Homes Standard, and the enforcement of the Fire Safety Act. No doubt this will also set back residential starts for the foreseeable future as developers seek to comply with tougher specification requirements.

“However, infrastructural investment does shine a light. It will help offset constrained activity with multi-billion pound projects including HS2, Hinkley Point C, as well as long-term frameworks activity in roads and energy. Hopefully, the Chancellor’s Spring Budget announcement next month will lay out more concrete details of the Government’s spending in these verticals.”

“However, infrastructural investment does shine a light. It will help offset constrained activity with multi-billion pound projects including HS2, Hinkley Point C, as well as long-term frameworks activity in roads and energy. Hopefully, the Chancellor’s Spring Budget announcement next month will lay out more concrete details of the Government’s spending in these verticals.”

The sector-specific and regional index, which measures underlying project performance, painted a picture of general decline. Project starts across almost every vertical falling in the three months to January plummeted.

Residential

Residential starts remained depressed at the outset of 2023, falling 26% during the index period to stand 38% lower than a year ago.

Private housing was 34% down on the previous year and 28% lower than the three months to January. It was an equally grim outlook for social housing, where project start levels dropped by a fifth compared to the preceding three months and plummeting by 49% against 2022 figures.

Non-Residential

Non-residential performance was weak. Particularly, industrial project-starts suffered a 34% fall during the three months to January, with levels almost slashed in half (45%) compared to last year.

Unsurprisingly, with discretionary spending at a low ebb, retail fared poorly with the value of project starts falling 29% against the preceding three months and 33% compared to the same period in 2022.

However, hotel and leisure starts on site actually increased by 16% against the preceding three months, indicating a very gradual return of consumer confidence. Likewise, healthcare grew by 16% in the three months to January, yet neither of these verticals were able to rise above 2022 levels.

Education project starts declined 19% against the previous three months and 31% compared to last year. Offices followed a similar trajectory, with the value of starts on site 7% lower than 2022 figures and 26% down on the three months to January 2023. Once again, community and amenity starts fell, posting a 27% drop on the preceding three months, slipping back by a quarter on the previous year.

Civils work starting on site stumbled, falling back 3% against the preceding three months, however the vertical recovered itself to stand 5% up on a year ago. Although utilities dipped 8% against the three months to January, figures rose by 26% compared to 2022. Infrastructure performance stagnated, remaining flat against the previous three months, registering a modest decline of 4% on last year.

Regional Performance

Regional performance was poor, with a couple of exceptions. The North East performed relatively well, with project-starts increasing 20% during the three months to January but remaining 16% down on the year before.

The South East followed a similar trend, with the value of project-starts advancing 19% against the preceding three months but remaining 9% behind the previous year.

London (-23%) and the South West (-24%) performed particularly poorly against the preceding three months, falling back 36% and 39% against a year ago, respectively.

Some regions fared worse still, including Scotland, where the value of project-starts fell 45% against the preceding three months to stand 42% down on the previous year’s levels.

The East Midlands, West Midlands and the North West also suffered falls in project-starts against both the preceding three months and previous year.

To find out more about Glenigan and its construction intelligence services click here.

.

{kind=link}